16. Endogenous Grid Method#

GPU

This lecture was built using a machine with access to a GPU — although it will also run without one.

Google Colab has a free tier with GPUs that you can access as follows:

Click on the “play” icon top right

Select Colab

Set the runtime environment to include a GPU

16.1. Overview#

In this lecture we use the endogenous grid method (EGM) to solve a basic income fluctuation (optimal savings) problem.

Background on the endogenous grid method can be found in an earlier QuantEcon lecture.

Here we focus on providing an efficient JAX implementation.

In addition to JAX and Anaconda, this lecture will need the following libraries:

!pip install --upgrade quantecon

import quantecon as qe

import matplotlib.pyplot as plt

import numpy as np

import jax

import jax.numpy as jnp

import numba

from time import time

Let’s check the GPU we are running

!nvidia-smi

Fri Jun 26 06:39:37 2026

+-----------------------------------------------------------------------------------------+

| NVIDIA-SMI 580.105.08 Driver Version: 580.105.08 CUDA Version: 13.0 |

+-----------------------------------------+------------------------+----------------------+

| GPU Name Persistence-M | Bus-Id Disp.A | Volatile Uncorr. ECC |

| Fan Temp Perf Pwr:Usage/Cap | Memory-Usage | GPU-Util Compute M. |

| | | MIG M. |

|=========================================+========================+======================|

| 0 Tesla T4 On | 00000000:00:1E.0 Off | 0 |

| N/A 34C P8 8W / 70W | 0MiB / 15360MiB | 0% Default |

| | | N/A |

+-----------------------------------------+------------------------+----------------------+

+-----------------------------------------------------------------------------------------+

| Processes: |

| GPU GI CI PID Type Process name GPU Memory |

| ID ID Usage |

|=========================================================================================|

| No running processes found |

+-----------------------------------------------------------------------------------------+

We use 64 bit floating point numbers for extra precision.

jax.config.update("jax_enable_x64", True)

16.2. Setup#

We consider a household that chooses a state-contingent consumption plan \(\{c_t\}_{t \geq 0}\) to maximize

subject to

Here \(R = 1 + r\) where \(r\) is the interest rate.

The income process \(\{Y_t\}\) is a Markov chain generated by stochastic matrix \(P\).

The matrix \(P\) and the grid of values taken by \(Y_t\) are obtained by discretizing the AR(1) process

where \(\{\epsilon_t\}\) is IID and standard normal.

Utility has the CRRA specification

The following function stores default parameter values for the income fluctuation problem and creates suitable arrays.

def ifp(R=1.01, # gross interest rate

β=0.99, # discount factor

γ=1.5, # CRRA preference parameter

s_max=16, # savings grid max

s_size=200, # savings grid size

ρ=0.99, # income persistence

ν=0.02, # income volatility

y_size=25): # income grid size

# require R β < 1 for convergence

assert R * β < 1, "Stability condition failed."

# Create income Markov chain

mc = qe.tauchen(y_size, ρ, ν)

y_grid, P = jnp.exp(mc.state_values), mc.P

# Shift to JAX arrays

P, y_grid = jax.device_put((P, y_grid))

s_grid = jnp.linspace(0, s_max, s_size)

# Pack and return

constants = β, R, γ

sizes = s_size, y_size

arrays = s_grid, y_grid, P

return constants, sizes, arrays

16.3. Solution method#

Let \(S = \mathbb R_+ \times \mathsf Y\) be the set of possible values for the state \((a_t, Y_t)\).

We aim to compute an optimal consumption policy \(\sigma^* \colon S \to \mathbb R\), under which dynamics are given by

In this section we discuss how we intend to solve for this policy.

16.3.1. Euler equation#

The Euler equation for the optimization problem is

An explanation for this expression can be found here.

We rewrite the Euler equation in functional form

where \((u' \circ \sigma)(a, y) := u'(\sigma(a, y))\) and \(\sigma\) is a consumption policy.

For given consumption policy \(\sigma\), we define \((K \sigma) (a,y)\) as the unique \(c \in [0, a]\) that solves

iterating with \(K\) computes an optimal policy and

if \(\sigma\) is increasing in its first argument, then so is \(K\sigma\)

Hence below we always assume that \(\sigma\) is increasing in its first argument.

The EGM is a technique for computing the update \(K\sigma\) given \(\sigma\) along a grid of asset values.

Notice that, since \(u'(a) \to \infty\) as \(a \downarrow 0\), the second term in the max in (16.1) dominates for sufficiently small \(a\).

Also, again using (16.1), we have \(c=a\) for all such \(a\).

Hence, for sufficiently small \(a\),

Equality holds at \(\bar a(y)\) given by

We can now write

Equivalently, we can state that the \(c\) satisfying \(c = (K\sigma)(a, y)\) obeys

We begin with an exogenous grid of saving values \(0 = s_0 < \ldots < s_{N-1}\)

Using the exogenous savings grid, and a fixed value of \(y\), we create an endogenous asset grid \(a_0, \ldots, a_{N-1}\) and a consumption grid \(c_0, \ldots, c_{N-1}\) as follows.

First we set \(a_0 = c_0 = 0\), since zero consumption is an optimal (in fact the only) choice when \(a=0\).

Then, for \(i > 0\), we compute

and we set

We claim that each pair \(a_i, c_i\) obeys (16.2).

Indeed, since \(s_i > 0\), choosing \(c_i\) according to (16.3) gives

where the inequality uses the fact that \(\sigma\) is increasing in its first argument.

If we now take \(a_i = s_i + c_i\) we get \(a_i > \bar a(y)\), so the pair \((a_i, c_i)\) satisfies

Hence (16.2) holds.

We are now ready to iterate with \(K\).

16.3.2. JAX version#

First we define a vectorized operator \(K\) based on the EGM.

Notice in the code below that

we avoid all loops and any mutation of arrays

the function is pure (no globals, no mutation of inputs)

def K_egm(a_in, σ_in, constants, sizes, arrays):

"""

The vectorized operator K using EGM.

"""

# Unpack

β, R, γ = constants

s_size, y_size = sizes

s_grid, y_grid, P = arrays

def u_prime(c):

return c**(-γ)

def u_prime_inv(u):

return u**(-1/γ)

# Linearly interpolate σ(a, y)

def σ(a, y):

return jnp.interp(a, a_in[:, y], σ_in[:, y])

σ_vec = jnp.vectorize(σ)

# Broadcast and vectorize

y_hat = jnp.reshape(y_grid, (1, 1, y_size))

y_hat_idx = jnp.reshape(jnp.arange(y_size), (1, 1, y_size))

s = jnp.reshape(s_grid, (s_size, 1, 1))

P = jnp.reshape(P, (1, y_size, y_size))

# Evaluate consumption choice

a_next = R * s + y_hat

σ_next = σ_vec(a_next, y_hat_idx)

up = u_prime(σ_next)

E = jnp.sum(up * P, axis=-1)

c = u_prime_inv(β * R * E)

# Set up a column vector with zero in the first row and ones elsewhere

e_0 = jnp.ones(s_size) - jnp.identity(s_size)[:, 0]

e_0 = jnp.reshape(e_0, (s_size, 1))

# The policy is computed consumption with the first row set to zero

σ_out = c * e_0

# Compute a_out by a = s + c

a_out = np.reshape(s_grid, (s_size, 1)) + σ_out

return a_out, σ_out

Then we use jax.jit to compile \(K\).

We use static_argnums to allow a recompile whenever sizes changes, since the compiler likes to specialize on shapes.

K_egm_jax = jax.jit(K_egm, static_argnums=(3,))

Next we define a successive approximator that repeatedly applies \(K\).

def successive_approx_jax(model,

tol=1e-5,

max_iter=100_000,

verbose=True,

print_skip=25):

# Unpack

constants, sizes, arrays = model

β, R, γ = constants

s_size, y_size = sizes

s_grid, y_grid, P = arrays

# Initial condition is to consume all in every state

σ_init = jnp.repeat(s_grid, y_size)

σ_init = jnp.reshape(σ_init, (s_size, y_size))

a_init = jnp.copy(σ_init)

a_vec, σ_vec = a_init, σ_init

i = 0

error = tol + 1

while i < max_iter and error > tol:

a_new, σ_new = K_egm_jax(a_vec, σ_vec, constants, sizes, arrays)

error = jnp.max(jnp.abs(σ_vec - σ_new))

i += 1

if verbose and i % print_skip == 0:

print(f"Error at iteration {i} is {error}.")

a_vec, σ_vec = jnp.copy(a_new), jnp.copy(σ_new)

if error > tol:

print("Failed to converge!")

else:

print(f"\nConverged in {i} iterations.")

return a_new, σ_new

16.3.3. Numba version#

Below we provide a second set of code, which solves the same model with Numba.

The purpose of this code is to cross-check our results from the JAX version, as well as to do a runtime comparison.

Most readers will want to skip ahead to the next section, where we solve the model and run the cross-check.

@numba.jit

def K_egm_nb(a_in, σ_in, constants, sizes, arrays):

"""

The operator K using Numba.

"""

# Simplify names

β, R, γ = constants

s_size, y_size = sizes

s_grid, y_grid, P = arrays

def u_prime(c):

return c**(-γ)

def u_prime_inv(u):

return u**(-1/γ)

# Linear interpolation of policy using endogenous grid

def σ(a, z):

return np.interp(a, a_in[:, z], σ_in[:, z])

# Allocate memory for new consumption array

σ_out = np.zeros_like(σ_in)

a_out = np.zeros_like(σ_out)

for i, s in enumerate(s_grid[1:]):

i += 1

for z in range(y_size):

expect = 0.0

for z_hat in range(y_size):

expect += u_prime(σ(R * s + y_grid[z_hat], z_hat)) * \

P[z, z_hat]

c = u_prime_inv(β * R * expect)

σ_out[i, z] = c

a_out[i, z] = s + c

return a_out, σ_out

def successive_approx_numba(model, # Class with model information

tol=1e-5,

max_iter=100_000,

verbose=True,

print_skip=25):

# Unpack

constants, sizes, arrays = model

s_size, y_size = sizes

# make NumPy versions of arrays

arrays = tuple(map(np.array, arrays))

s_grid, y_grid, P = arrays

σ_init = np.repeat(s_grid, y_size)

σ_init = np.reshape(σ_init, (s_size, y_size))

a_init = np.copy(σ_init)

a_vec, σ_vec = a_init, σ_init

# Set up loop

i = 0

error = tol + 1

while i < max_iter and error > tol:

a_new, σ_new = K_egm_nb(a_vec, σ_vec, constants, sizes, arrays)

error = np.max(np.abs(σ_vec - σ_new))

i += 1

if verbose and i % print_skip == 0:

print(f"Error at iteration {i} is {error}.")

a_vec, σ_vec = np.copy(a_new), np.copy(σ_new)

if error > tol:

print("Failed to converge!")

else:

print(f"\nConverged in {i} iterations.")

return a_new, σ_new

16.4. Solutions#

Here we solve the IFP with JAX and Numba.

We will compare both the outputs and the execution time.

16.4.1. Outputs#

model = ifp()

Here’s a first run of the JAX code.

%%time

a_star_egm_jax, σ_star_egm_jax = successive_approx_jax(model,

print_skip=1000)

Error at iteration 1000 is 6.472028596182788e-05.

Error at iteration 2000 is 1.2994575430580468e-05.

Converged in 2192 iterations.

CPU times: user 3.87 s, sys: 1.1 s, total: 4.97 s

Wall time: 3.32 s

Next let’s solve the same IFP with Numba.

%%time

a_star_egm_nb, σ_star_egm_nb = successive_approx_numba(model,

print_skip=1000)

Error at iteration 1000 is 6.472028596182788e-05.

Error at iteration 2000 is 1.2994575430802513e-05.

Converged in 2192 iterations.

CPU times: user 1min 14s, sys: 0 ns, total: 1min 14s

Wall time: 1min 14s

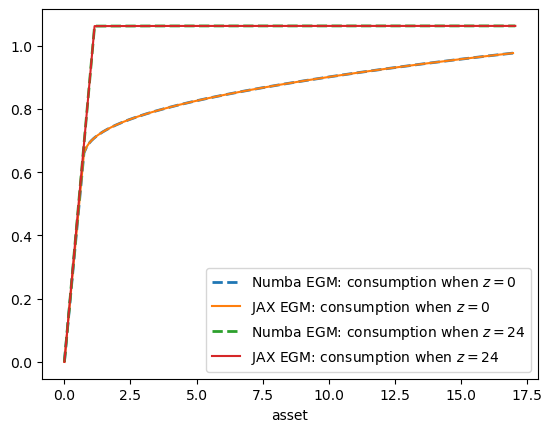

Now let’s check the outputs in a plot to make sure they are the same.

constants, sizes, arrays = model

β, R, γ = constants

s_size, y_size = sizes

s_grid, y_grid, P = arrays

fig, ax = plt.subplots()

for z in (0, y_size-1):

ax.plot(a_star_egm_nb[:, z],

σ_star_egm_nb[:, z],

'--', lw=2,

label=f"Numba EGM: consumption when $z={z}$")

ax.plot(a_star_egm_jax[:, z],

σ_star_egm_jax[:, z],

label=f"JAX EGM: consumption when $z={z}$")

ax.set_xlabel('asset')

plt.legend()

plt.show()

16.4.2. Timing#

Now let’s compare execution time of the two methods.

start = time()

a_star_egm_jax, σ_star_egm_jax = successive_approx_jax(model,

print_skip=1000)

jax_time_without_compile = time() - start

print("Jax execution time = ", jax_time_without_compile)

Error at iteration 1000 is 6.472028596182788e-05.

Error at iteration 2000 is 1.2994575430580468e-05.

Converged in 2192 iterations.

Jax execution time = 2.4887890815734863

start = time()

a_star_egm_nb, σ_star_egm_nb = successive_approx_numba(model,

print_skip=1000)

numba_time_without_compile = time() - start

print("Numba execution time = ", numba_time_without_compile)

Error at iteration 1000 is 6.472028596182788e-05.

Error at iteration 2000 is 1.2994575430802513e-05.

Converged in 2192 iterations.

Numba execution time = 73.42691946029663

jax_time_without_compile / numba_time_without_compile

0.033894777281501275

The JAX code is significantly faster, as expected.

This difference will increase when more features (and state variables) are added to the model.