6. Kesten Processes and Firm Dynamics#

GPU

This lecture was built using a machine with access to a GPU — although it will also run without one.

Google Colab has a free tier with GPUs that you can access as follows:

Click on the “play” icon top right

Select Colab

Set the runtime environment to include a GPU

In addition to JAX and Anaconda, this lecture will need the following libraries:

!pip install quantecon

6.1. Overview#

This lecture describes Kesten processes, which are an important class of stochastic processes, and an application of firm dynamics.

The lecture draws on an earlier QuantEcon lecture, which uses Numba to accelerate the computations.

In that earlier lecture you can find a more detailed discussion of the concepts involved.

This lecture focuses on implementing the same computations in JAX.

Let’s start with some imports:

import matplotlib.pyplot as plt

import quantecon as qe

import jax

import jax.numpy as jnp

from jax import random

from jax import lax

from quantecon import tic, toc

from typing import NamedTuple

from functools import partial

Let’s check the GPU we are running

!nvidia-smi

Thu Jul 9 05:41:46 2026

+-----------------------------------------------------------------------------------------+

| NVIDIA-SMI 580.105.08 Driver Version: 580.105.08 CUDA Version: 13.0 |

+-----------------------------------------+------------------------+----------------------+

| GPU Name Persistence-M | Bus-Id Disp.A | Volatile Uncorr. ECC |

| Fan Temp Perf Pwr:Usage/Cap | Memory-Usage | GPU-Util Compute M. |

| | | MIG M. |

|=========================================+========================+======================|

| 0 Tesla T4 On | 00000000:00:1E.0 Off | 0 |

| N/A 37C P8 13W / 70W | 0MiB / 15360MiB | 0% Default |

| | | N/A |

+-----------------------------------------+------------------------+----------------------+

+-----------------------------------------------------------------------------------------+

| Processes: |

| GPU GI CI PID Type Process name GPU Memory |

| ID ID Usage |

|=========================================================================================|

| No running processes found |

+-----------------------------------------------------------------------------------------+

6.2. Kesten processes#

A Kesten process is a stochastic process of the form

where \(\{a_t\}_{t \geq 1}\) and \(\{\eta_t\}_{t \geq 1}\) are IID sequences.

We are interested in the dynamics of \(\{X_t\}_{t \geq 0}\) when \(X_0\) is given.

We will focus on the nonnegative scalar case, where \(X_t\) takes values in \(\mathbb R_+\).

In particular, we will assume that

the initial condition \(X_0\) is nonnegative,

\(\{a_t\}_{t \geq 1}\) is a nonnegative IID stochastic process and

\(\{\eta_t\}_{t \geq 1}\) is another nonnegative IID stochastic process, independent of the first.

6.2.1. Application: firm dynamics#

In this section we apply Kesten process theory to the study of firm dynamics.

6.2.1.1. Gibrat’s law#

It was postulated many years ago by Robert Gibrat that firm size evolves according to a simple rule whereby size next period is proportional to current size.

This is now known as Gibrat’s law of proportional growth.

We can express this idea by stating that a suitably defined measure \(s_t\) of firm size obeys

for some positive IID sequence \(\{a_t\}\).

Subsequent empirical research has shown that this specification is not accurate, particularly for small firms.

However, we can get close to the data by modifying (6.2) to

where \(\{a_t\}\) and \(\{b_t\}\) are both IID and independent of each other.

We now study the implications of this specification.

6.2.1.2. Heavy tails#

If the conditions of the Kesten–Goldie Theorem are satisfied, then (6.3) implies that the firm size distribution will have Pareto tails.

This matches empirical findings across many data sets.

But there is another unrealistic aspect of the firm dynamics specified in (6.3) that we need to address: it ignores entry and exit.

In any given period and in any given market, we observe significant numbers of firms entering and exiting the market.

In this setting, firm dynamics can be expressed as

The motivation behind and interpretation of (6.4) can be found in our earlier Kesten process lecture.

What can we say about dynamics?

Although (6.4) is not a Kesten process, it does update in the same way as a Kesten process when \(s_t\) is large.

So perhaps its stationary distribution still has Pareto tails?

We can investigate this question via simulation and rank-size plots.

The approach will be to

generate \(M\) draws of \(s_T\) when \(M\) and \(T\) are large and

plot the largest 1,000 of the resulting draws in a rank-size plot.

(The distribution of \(s_T\) will be close to the stationary distribution when \(T\) is large.)

In the simulation, we assume that each of \(a_t, b_t\) and \(e_t\) is lognormal.

Here’s a class to store parameters:

class Firm(NamedTuple):

μ_a: float = -0.5

σ_a: float = 0.1

μ_b: float = 0.0

σ_b: float = 0.5

μ_e: float = 0.0

σ_e: float = 0.5

s_bar: float = 1.0

Here’s code to update a cross-section of firms according to the dynamics in (6.4).

@jax.jit

def update_cross_section(s, a, b, e, firm):

μ_a, σ_a, μ_b, σ_b, μ_e, σ_e, s_bar = firm

s = jnp.where(s < s_bar, e, a * s + b)

return s

Now we write a for loop that repeatedly calls this function, to push a cross-section of firms forward in time.

For sufficiently large T, the cross-section it returns (the cross-section at

time T) corresponds to firm size distribution in (approximate) equilibrium.

def generate_cross_section(

firm, M=500_000, T=500, s_init=1.0, seed=123

):

μ_a, σ_a, μ_b, σ_b, μ_e, σ_e, s_bar = firm

key = random.key(seed)

# Initialize the cross-section to a common value

s = jnp.full((M, ), s_init)

# Perform updates on s for time t

for t in range(T):

key, *subkeys = random.split(key, 4)

a = μ_a + σ_a * random.normal(subkeys[0], (M,))

b = μ_b + σ_b * random.normal(subkeys[1], (M,))

e = μ_e + σ_e * random.normal(subkeys[2], (M,))

# Exponentiate shocks

a, b, e = jax.tree.map(jnp.exp, (a, b, e))

# Update the cross-section of firms

s = update_cross_section(s, a, b, e, firm)

return s

Let’s try running the code and generating a cross-section.

firm = Firm()

tic()

data = generate_cross_section(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:2.32

2.325608253479004

We run the function again so we can see the speed without compile time.

tic()

data = generate_cross_section(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:0.86

0.8644239902496338

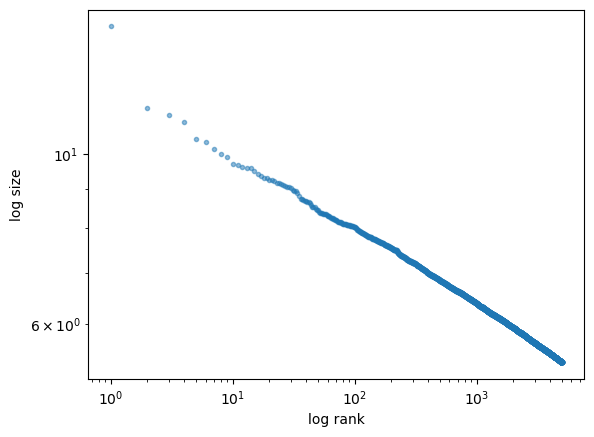

Let’s produce the rank-size plot and check the distribution:

fig, ax = plt.subplots()

rank_data, size_data = qe.rank_size(data, c=0.01)

ax.loglog(rank_data, size_data, 'o', markersize=3.0, alpha=0.5)

ax.set_xlabel("log rank")

ax.set_ylabel("log size")

plt.show()

The plot produces a straight line, consistent with a Pareto tail.

6.2.1.3. Alternative implementation with lax.fori_loop#

Although we JIT-compiled some of the code above,

we did not JIT-compile the for loop.

Let’s try squeezing out a bit more speed by

replacing the

forloop withlax.fori_loopandJIT-compiling the whole function.

Here is the lax.fori_loop version:

@partial(jax.jit, static_argnames=("T", "M"))

def generate_cross_section_lax(

firm, T=500, M=500_000, s_init=1.0, seed=123

):

μ_a, σ_a, μ_b, σ_b, μ_e, σ_e, s_bar = firm

key = random.key(seed)

# Initial cross section

s = jnp.full((M, ), s_init)

def update_cross_section(t, state):

s, key = state

key, *subkeys = jax.random.split(key, 4)

# Generate current random draws

a = μ_a + σ_a * random.normal(subkeys[0], (M,))

b = μ_b + σ_b * random.normal(subkeys[1], (M,))

e = μ_e + σ_e * random.normal(subkeys[2], (M,))

# Exponentiate them

a, b, e = jax.tree.map(jnp.exp, (a, b, e))

# Update the cross-section of firms

s = jnp.where(s < s_bar, e, a * s + b)

new_state = s, key

return new_state

# Use fori_loop

initial_state = s, key

final_s, final_key = lax.fori_loop(

0, T, update_cross_section, initial_state

)

return final_s

Let’s see if we get any speed gain

tic()

data = generate_cross_section_lax(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:1.13

1.1330854892730713

tic()

data = generate_cross_section_lax(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:0.06

0.06241130828857422

Here we produce the same rank-size plot:

fig, ax = plt.subplots()

rank_data, size_data = qe.rank_size(data, c=0.01)

ax.loglog(rank_data, size_data, 'o', markersize=3.0, alpha=0.5)

ax.set_xlabel("log rank")

ax.set_ylabel("log size")

plt.show()

6.3. Exercises#

Exercise 6.1

Try writing an alternative version of generate_cross_section_lax() where the entire sequence of random draws is generated at once, so that all of a, b, and e are of shape (T, M).

(The update_cross_section() function should not generate any random numbers.)

Does it improve the runtime?

What are the pros and cons of this approach?

Solution

@partial(jax.jit, static_argnames=("T", "M"))

def generate_cross_section_lax(

firm, T=500, M=500_000, s_init=1.0, seed=123

):

μ_a, σ_a, μ_b, σ_b, μ_e, σ_e, s_bar = firm

key = random.key(seed)

subkey_1, subkey_2, subkey_3 = random.split(key, 3)

# Generate entire sequence of random draws

a = μ_a + σ_a * random.normal(subkey_1, (T, M))

b = μ_b + σ_b * random.normal(subkey_2, (T, M))

e = μ_e + σ_e * random.normal(subkey_3, (T, M))

# Exponentiate them

a, b, e = jax.tree.map(jnp.exp, (a, b, e))

# Initial cross section

s = jnp.full((M, ), s_init)

def update_cross_section(t, s):

# Pull out the t-th cross-section of shocks

a_t, b_t, e_t = a[t], b[t], e[t]

s = jnp.where(s < s_bar, e_t, a_t * s + b_t)

return s

# Use lax.fori_loop to perform the calculations on all states

s_final = lax.fori_loop(0, T, update_cross_section, s)

return s_final

Here are the run times.

tic()

data = generate_cross_section_lax(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:1.07

1.0745184421539307

tic()

data = generate_cross_section_lax(firm).block_until_ready()

toc()

TOC: Elapsed: 0:00:0.07

0.07181167602539062

This method might or might not be faster.

In general, the relative speed will depend on the size of the cross-section and the length of the simulation paths.

However, this method is far more memory intensive.

It will fail when \(T\) and \(M\) become sufficiently large.