11. Optimal Savings I: Value Function Iteration#

GPU

This lecture was built using a machine with access to a GPU — although it will also run without one.

Google Colab has a free tier with GPUs that you can access as follows:

Click on the “play” icon top right

Select Colab

Set the runtime environment to include a GPU

In addition to JAX and Anaconda, this lecture will need the following libraries:

!pip install quantecon

We will use the following imports:

import quantecon as qe

import numpy as np

import jax

import jax.numpy as jnp

import matplotlib.pyplot as plt

from collections import namedtuple

from time import time

Let’s check the GPU we are running

!nvidia-smi

Fri Jun 26 06:48:36 2026

+-----------------------------------------------------------------------------------------+

| NVIDIA-SMI 580.105.08 Driver Version: 580.105.08 CUDA Version: 13.0 |

+-----------------------------------------+------------------------+----------------------+

| GPU Name Persistence-M | Bus-Id Disp.A | Volatile Uncorr. ECC |

| Fan Temp Perf Pwr:Usage/Cap | Memory-Usage | GPU-Util Compute M. |

| | | MIG M. |

|=========================================+========================+======================|

| 0 Tesla T4 On | 00000000:00:1E.0 Off | 0 |

| N/A 35C P8 13W / 70W | 0MiB / 15360MiB | 0% Default |

| | | N/A |

+-----------------------------------------+------------------------+----------------------+

+-----------------------------------------------------------------------------------------+

| Processes: |

| GPU GI CI PID Type Process name GPU Memory |

| ID ID Usage |

|=========================================================================================|

| No running processes found |

+-----------------------------------------------------------------------------------------+

We’ll use 64 bit floats to gain extra precision.

jax.config.update("jax_enable_x64", True)

11.1. Overview#

We consider an optimal savings problem with CRRA utility and budget constraint

where

\(C_t\) is consumption and \(C_t \geq 0\),

\(W_t\) is wealth and \(W_t \geq 0\),

\(R > 0\) is a gross rate of return, and

\((Y_t)\) is labor income.

We assume below that labor income is a discretized AR(1) process.

The Bellman equation is

where

In the code we use the function

the encapsulate the right hand side of the Bellman equation.

11.2. Starting with NumPy#

Let’s start with a standard NumPy version running on the CPU.

Starting with this traditional approach will allow us to record the speed gain associated with switching to JAX.

(NumPy operations are similar to MATLAB operations, so this also serves as a rough comparison with MATLAB.)

11.2.1. Functions and operators#

The following function contains default parameters and returns tuples that contain the key computational components of the model.

def create_consumption_model(R=1.01, # Gross interest rate

β=0.98, # Discount factor

γ=2, # CRRA parameter

w_min=0.01, # Min wealth

w_max=5.0, # Max wealth

w_size=150, # Grid side

ρ=0.9, ν=0.1, y_size=100): # Income parameters

"""

A function that takes in parameters and returns parameters and grids

for the optimal savings problem.

"""

# Build grids and transition probabilities

w_grid = np.linspace(w_min, w_max, w_size)

mc = qe.tauchen(n=y_size, rho=ρ, sigma=ν)

y_grid, Q = np.exp(mc.state_values), mc.P

# Pack and return

params = β, R, γ

sizes = w_size, y_size

arrays = w_grid, y_grid, Q

return params, sizes, arrays

(The function returns sizes of arrays because we use them later to help compile functions in JAX.)

To produce efficient NumPy code, we will use a vectorized approach.

The first step is to create the right hand side of the Bellman equation as a multi-dimensional array with dimensions over all states and controls.

def B(v, params, sizes, arrays):

"""

A vectorized version of the right-hand side of the Bellman equation

(before maximization), which is a 3D array representing

B(w, y, w′) = u(Rw + y - w′) + β Σ_y′ v(w′, y′) Q(y, y′)

for all (w, y, w′).

"""

# Unpack

β, R, γ = params

w_size, y_size = sizes

w_grid, y_grid, Q = arrays

# Compute current rewards r(w, y, wp) as array r[i, j, ip]

w = np.reshape(w_grid, (w_size, 1, 1)) # w[i] -> w[i, j, ip]

y = np.reshape(y_grid, (1, y_size, 1)) # z[j] -> z[i, j, ip]

wp = np.reshape(w_grid, (1, 1, w_size)) # wp[ip] -> wp[i, j, ip]

c = R * w + y - wp

# Calculate continuation rewards at all combinations of (w, y, wp)

v = np.reshape(v, (1, 1, w_size, y_size)) # v[ip, jp] -> v[i, j, ip, jp]

Q = np.reshape(Q, (1, y_size, 1, y_size)) # Q[j, jp] -> Q[i, j, ip, jp]

EV = np.sum(v * Q, axis=3) # sum over last index jp

# Compute the right-hand side of the Bellman equation

return np.where(c > 0, c**(1-γ)/(1-γ) + β * EV, -np.inf)

Here are two functions we need for value function iteration.

The first is the Bellman operator.

The second computes a \(v\)-greedy policy given \(v\) (i.e., the policy that maximizes the right-hand side of the Bellman equation.)

def T(v, params, sizes, arrays):

"The Bellman operator."

return np.max(B(v, params, sizes, arrays), axis=2)

def get_greedy(v, params, sizes, arrays):

"Computes a v-greedy policy, returned as a set of indices."

return np.argmax(B(v, params, sizes, arrays), axis=2)

11.2.2. Value function iteration#

Here’s a routine that performs value function iteration.

def value_function_iteration(model, max_iter=10_000, tol=1e-5):

params, sizes, arrays = model

v = np.zeros(sizes)

i, error = 0, tol + 1

while error > tol and i < max_iter:

v_new = T(v, params, sizes, arrays)

error = np.max(np.abs(v_new - v))

i += 1

v = v_new

return v, get_greedy(v, params, sizes, arrays)

Now we create an instance, unpack it, and test how long it takes to solve the model.

model = create_consumption_model()

# Unpack

params, sizes, arrays = model

β, R, γ = params

w_size, y_size = sizes

w_grid, y_grid, Q = arrays

print("Starting VFI.")

start = time()

v_star, σ_star = value_function_iteration(model)

numpy_with_compile = time() - start

print(f"VFI completed in {numpy_with_compile} seconds.")

Starting VFI.

VFI completed in 17.15130591392517 seconds.

Let’s run it again to eliminate compile time.

start = time()

v_star, σ_star = value_function_iteration(model)

numpy_without_compile = time() - start

print(f"VFI completed in {numpy_without_compile} seconds.")

VFI completed in 17.800621271133423 seconds.

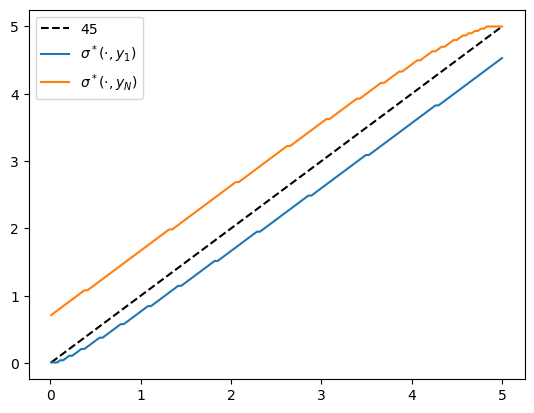

Here’s a plot of the policy function.

fig, ax = plt.subplots()

ax.plot(w_grid, w_grid, "k--", label="45")

ax.plot(w_grid, w_grid[σ_star[:, 1]], label="$\\sigma^*(\cdot, y_1)$")

ax.plot(w_grid, w_grid[σ_star[:, -1]], label="$\\sigma^*(\cdot, y_N)$")

ax.legend()

plt.show()

Fig. 11.1 Policy function#

11.3. Switching to JAX#

To switch over to JAX, we change np to jnp throughout and add some

jax.jit requests.

11.3.1. Functions and operators#

We redefine create_consumption_model to produce JAX arrays.

def create_consumption_model(R=1.01, # Gross interest rate

β=0.98, # Discount factor

γ=2, # CRRA parameter

w_min=0.01, # Min wealth

w_max=5.0, # Max wealth

w_size=150, # Grid side

ρ=0.9, ν=0.1, y_size=100): # Income parameters

"""

A function that takes in parameters and returns parameters and grids

for the optimal savings problem.

"""

w_grid = jnp.linspace(w_min, w_max, w_size)

mc = qe.tauchen(n=y_size, rho=ρ, sigma=ν)

y_grid, Q = jnp.exp(mc.state_values), jax.device_put(mc.P)

sizes = w_size, y_size

return (β, R, γ), sizes, (w_grid, y_grid, Q)

The right hand side of the Bellman equation is the same as the NumPy version

after switching np to jnp.

def B(v, params, sizes, arrays):

"""

A vectorized version of the right-hand side of the Bellman equation

(before maximization), which is a 3D array representing

B(w, y, w′) = u(Rw + y - w′) + β Σ_y′ v(w′, y′) Q(y, y′)

for all (w, y, w′).

"""

# Unpack

β, R, γ = params

w_size, y_size = sizes

w_grid, y_grid, Q = arrays

# Compute current rewards r(w, y, wp) as array r[i, j, ip]

w = jnp.reshape(w_grid, (w_size, 1, 1)) # w[i] -> w[i, j, ip]

y = jnp.reshape(y_grid, (1, y_size, 1)) # z[j] -> z[i, j, ip]

wp = jnp.reshape(w_grid, (1, 1, w_size)) # wp[ip] -> wp[i, j, ip]

c = R * w + y - wp

# Calculate continuation rewards at all combinations of (w, y, wp)

v = jnp.reshape(v, (1, 1, w_size, y_size)) # v[ip, jp] -> v[i, j, ip, jp]

Q = jnp.reshape(Q, (1, y_size, 1, y_size)) # Q[j, jp] -> Q[i, j, ip, jp]

EV = jnp.sum(v * Q, axis=3) # sum over last index jp

# Compute the right-hand side of the Bellman equation

return jnp.where(c > 0, c**(1-γ)/(1-γ) + β * EV, -jnp.inf)

Some readers might be concerned that we are creating high dimensional arrays, leading to inefficiency.

Could they be avoided by more careful vectorization?

In fact this is not necessary: this function will be JIT-compiled by JAX, and the JIT compiler will optimize compiled code to minimize memory use.

B = jax.jit(B, static_argnums=(2,))

In the call above, we indicate to the compiler that sizes is static, so the

compiler can parallelize optimally while taking array sizes as fixed.

The Bellman operator \(T\) can be implemented by

def T(v, params, sizes, arrays):

"The Bellman operator."

return jnp.max(B(v, params, sizes, arrays), axis=2)

T = jax.jit(T, static_argnums=(2,))

The next function computes a \(v\)-greedy policy given \(v\) (i.e., the policy that maximizes the right-hand side of the Bellman equation.)

def get_greedy(v, params, sizes, arrays):

"Computes a v-greedy policy, returned as a set of indices."

return jnp.argmax(B(v, params, sizes, arrays), axis=2)

get_greedy = jax.jit(get_greedy, static_argnums=(2,))

11.3.2. Successive approximation#

Now we define a solver that implements VFI.

We could use the one we built for NumPy above, after changing np to jnp.

Alternatively, we can push a bit harder and write a compiled version using

jax.lax.while_loop.

This will give us just a bit more speed.

The first step is to write a compiled successive approximation routine that

performs fixed point iteration on some given function T.

def successive_approx_jax(T, # Operator (callable)

x_0, # Initial condition

tolerance=1e-6, # Error tolerance

max_iter=10_000): # Max iteration bound

def body_fun(k_x_err):

k, x, error = k_x_err

x_new = T(x)

error = jnp.max(jnp.abs(x_new - x))

return k + 1, x_new, error

def cond_fun(k_x_err):

k, x, error = k_x_err

return jnp.logical_and(error > tolerance, k < max_iter)

k, x, error = jax.lax.while_loop(cond_fun, body_fun,

(1, x_0, tolerance + 1))

return x

successive_approx_jax = \

jax.jit(successive_approx_jax, static_argnums=(0,))

Our value function iteration routine calls successive_approx_jax while passing

in the Bellman operator.

def value_function_iteration(model, tol=1e-5):

params, sizes, arrays = model

vz = jnp.zeros(sizes)

_T = lambda v: T(v, params, sizes, arrays)

v_star = successive_approx_jax(_T, vz, tolerance=tol)

return v_star, get_greedy(v_star, params, sizes, arrays)

11.3.3. Timing#

Let’s create an instance and unpack it.

model = create_consumption_model()

# Unpack

params, sizes, arrays = model

β, R, γ = params

w_size, y_size = sizes

w_grid, y_grid, Q = arrays

Let’s see how long it takes to solve this model.

print("Starting VFI using vectorization.")

start = time()

v_star_jax, σ_star_jax = value_function_iteration(model)

jax_with_compile = time() - start

print(f"VFI completed in {jax_with_compile} seconds.")

Starting VFI using vectorization.

VFI completed in 0.8195633888244629 seconds.

Let’s run it again to eliminate compile time.

start = time()

v_star_jax, σ_star_jax = value_function_iteration(model)

jax_without_compile = time() - start

print(f"VFI completed in {jax_without_compile} seconds.")

VFI completed in 0.3641531467437744 seconds.

The relative speed gain is

print(f"Relative speed gain = {numpy_without_compile / jax_without_compile}")

Relative speed gain = 48.882239327889984

This is an impressive speed up and in fact we can do better still by switching to alternative algorithms that are better suited to parallelization.

These algorithms are discussed in a separate lecture.

11.4. Switching to vmap#

Before we discuss alternative algorithms, let’s take another look at value function iteration.

For this simple optimal savings problem, direct vectorization is relatively easy.

In particular, it’s straightforward to express the right hand side of the Bellman equation as an array that stores evaluations of the function at every state and control.

For more complex models direct vectorization can be much harder.

For this reason, it helps to have another approach to fast JAX implementations up our sleeves.

Here’s a version that

writes the right hand side of the Bellman operator as a function of individual states and controls, and

applies

jax.vmapon the outside to achieve a parallelized solution.

First let’s rewrite B

def B(v, params, arrays, i, j, ip):

"""

The right-hand side of the Bellman equation before maximization, which takes

the form

B(w, y, w′) = u(Rw + y - w′) + β Σ_y′ v(w′, y′) Q(y, y′)

The indices are (i, j, ip) -> (w, y, w′).

"""

β, R, γ = params

w_grid, y_grid, Q = arrays

w, y, wp = w_grid[i], y_grid[j], w_grid[ip]

c = R * w + y - wp

EV = jnp.sum(v[ip, :] * Q[j, :])

return jnp.where(c > 0, c**(1-γ)/(1-γ) + β * EV, -jnp.inf)

Now we successively apply vmap to simulate nested loops.

B_1 = jax.vmap(B, in_axes=(None, None, None, None, None, 0))

B_2 = jax.vmap(B_1, in_axes=(None, None, None, None, 0, None))

B_vmap = jax.vmap(B_2, in_axes=(None, None, None, 0, None, None))

Here’s the Bellman operator and the get_greedy functions for the vmap case.

def T_vmap(v, params, sizes, arrays):

"The Bellman operator."

w_size, y_size = sizes

w_indices, y_indices = jnp.arange(w_size), jnp.arange(y_size)

B_values = B_vmap(v, params, arrays, w_indices, y_indices, w_indices)

return jnp.max(B_values, axis=-1)

T_vmap = jax.jit(T_vmap, static_argnums=(2,))

def get_greedy_vmap(v, params, sizes, arrays):

"Computes a v-greedy policy, returned as a set of indices."

w_size, y_size = sizes

w_indices, y_indices = jnp.arange(w_size), jnp.arange(y_size)

B_values = B_vmap(v, params, arrays, w_indices, y_indices, w_indices)

return jnp.argmax(B_values, axis=-1)

get_greedy_vmap = jax.jit(get_greedy_vmap, static_argnums=(2,))

Here’s the iteration routine.

def value_iteration_vmap(model, tol=1e-5):

params, sizes, arrays = model

vz = jnp.zeros(sizes)

_T = lambda v: T_vmap(v, params, sizes, arrays)

v_star = successive_approx_jax(_T, vz, tolerance=tol)

return v_star, get_greedy(v_star, params, sizes, arrays)

Let’s see how long it takes to solve the model using the vmap method.

print("Starting VFI using vmap.")

start = time()

v_star_vmap, σ_star_vmap = value_iteration_vmap(model)

jax_vmap_with_compile = time() - start

print(f"VFI completed in {jax_vmap_with_compile} seconds.")

Starting VFI using vmap.

VFI completed in 0.5037593841552734 seconds.

Let’s run it again to get rid of compile time.

start = time()

v_star_vmap, σ_star_vmap = value_iteration_vmap(model)

jax_vmap_without_compile = time() - start

print(f"VFI completed in {jax_vmap_without_compile} seconds.")

VFI completed in 0.3999595642089844 seconds.

We need to make sure that we got the same result.

print(jnp.allclose(v_star_vmap, v_star_jax))

print(jnp.allclose(σ_star_vmap, σ_star_jax))

True

True

Here’s the speed gain associated with switching from the NumPy version to JAX with vmap:

print(f"Relative speed = {numpy_without_compile/jax_vmap_without_compile}")

Relative speed = 44.506052271405

And here’s the comparison with the first JAX implementation (which used direct vectorization).

print(f"Relative speed = {jax_without_compile / jax_vmap_without_compile}")

Relative speed = 0.9104749062920255

The execution times for the two JAX versions are relatively similar.

However, as emphasized above, having a second method up our sleeves (i.e, the

vmap approach) will be helpful when confronting dynamic programs with more

sophisticated Bellman equations.