14. Optimal Investment#

GPU

This lecture was built using a machine with access to a GPU — although it will also run without one.

Google Colab has a free tier with GPUs that you can access as follows:

Click on the “play” icon top right

Select Colab

Set the runtime environment to include a GPU

In addition to JAX and Anaconda, this lecture will need the following libraries:

!pip install --upgrade quantecon

We study a monopolist who faces inverse demand curve

where

\(P_t\) is price,

\(Y_t\) is output and

\(Z_t\) is a demand shock.

We assume that \(Z_t\) is a discretized AR(1) process, specified below.

Current profits are

Combining with the demand curve and writing \(y, y'\) for \(Y_t, Y_{t+1}\), this becomes

The firm maximizes present value of expected discounted profits. The Bellman equation is

We discretize \(y\) to a finite grid y_grid.

In essence, the firm tries to choose output close to the monopolist profit maximizer, given \(Z_t\), but is constrained by adjustment costs.

Let’s begin with the following imports

import quantecon as qe

import jax

import jax.numpy as jnp

import matplotlib.pyplot as plt

from time import time

Let’s check the GPU we are running

!nvidia-smi

Fri Jun 26 06:48:14 2026

+-----------------------------------------------------------------------------------------+

| NVIDIA-SMI 580.105.08 Driver Version: 580.105.08 CUDA Version: 13.0 |

+-----------------------------------------+------------------------+----------------------+

| GPU Name Persistence-M | Bus-Id Disp.A | Volatile Uncorr. ECC |

| Fan Temp Perf Pwr:Usage/Cap | Memory-Usage | GPU-Util Compute M. |

| | | MIG M. |

|=========================================+========================+======================|

| 0 Tesla T4 On | 00000000:00:1E.0 Off | 0 |

| N/A 31C P8 13W / 70W | 0MiB / 15360MiB | 0% Default |

| | | N/A |

+-----------------------------------------+------------------------+----------------------+

+-----------------------------------------------------------------------------------------+

| Processes: |

| GPU GI CI PID Type Process name GPU Memory |

| ID ID Usage |

|=========================================================================================|

| No running processes found |

+-----------------------------------------------------------------------------------------+

We will use 64 bit floats with JAX in order to increase the precision.

jax.config.update("jax_enable_x64", True)

Let’s define a function to create an investment model using the given parameters.

def create_investment_model(

r=0.01, # Interest rate

a_0=10.0, a_1=1.0, # Demand parameters

γ=25.0, c=1.0, # Adjustment and unit cost

y_min=0.0, y_max=20.0, y_size=100, # Grid for output

ρ=0.9, ν=1.0, # AR(1) parameters

z_size=150): # Grid size for shock

"""

A function that takes in parameters and returns an instance of Model that

contains data for the investment problem.

"""

β = 1 / (1 + r)

y_grid = jnp.linspace(y_min, y_max, y_size)

mc = qe.tauchen(z_size, ρ, ν)

z_grid, Q = mc.state_values, mc.P

# Break up parameters into static and nonstatic components

constants = β, a_0, a_1, γ, c

sizes = y_size, z_size

arrays = y_grid, z_grid, Q

# Shift arrays to the device (e.g., GPU)

arrays = tuple(map(jax.device_put, arrays))

return constants, sizes, arrays

Let’s re-write the vectorized version of the right-hand side of the Bellman equation (before maximization), which is a 3D array representing

for all \((y, z, y')\).

def B(v, constants, sizes, arrays):

"""

A vectorized version of the right-hand side of the Bellman equation

(before maximization)

"""

# Unpack

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

# Compute current rewards r(y, z, yp) as array r[i, j, ip]

y = jnp.reshape(y_grid, (y_size, 1, 1)) # y[i] -> y[i, j, ip]

z = jnp.reshape(z_grid, (1, z_size, 1)) # z[j] -> z[i, j, ip]

yp = jnp.reshape(y_grid, (1, 1, y_size)) # yp[ip] -> yp[i, j, ip]

r = (a_0 - a_1 * y + z - c) * y - γ * (yp - y)**2

# Calculate continuation rewards at all combinations of (y, z, yp)

v = jnp.reshape(v, (1, 1, y_size, z_size)) # v[ip, jp] -> v[i, j, ip, jp]

Q = jnp.reshape(Q, (1, z_size, 1, z_size)) # Q[j, jp] -> Q[i, j, ip, jp]

EV = jnp.sum(v * Q, axis=3) # sum over last index jp

# Compute the right-hand side of the Bellman equation

return r + β * EV

# Create a jitted function

B = jax.jit(B, static_argnums=(2,))

We define a function to compute the current rewards \(r_\sigma\) given policy \(\sigma\), which is defined as the vector

def compute_r_σ(σ, constants, sizes, arrays):

"""

Compute the array r_σ[i, j] = r[i, j, σ[i, j]], which gives current

rewards given policy σ.

"""

# Unpack model

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

# Compute r_σ[i, j]

y = jnp.reshape(y_grid, (y_size, 1))

z = jnp.reshape(z_grid, (1, z_size))

yp = y_grid[σ]

r_σ = (a_0 - a_1 * y + z - c) * y - γ * (yp - y)**2

return r_σ

# Create the jitted function

compute_r_σ = jax.jit(compute_r_σ, static_argnums=(2,))

Define the Bellman operator.

def T(v, constants, sizes, arrays):

"""The Bellman operator."""

return jnp.max(B(v, constants, sizes, arrays), axis=2)

T = jax.jit(T, static_argnums=(2,))

The following function computes a v-greedy policy.

def get_greedy(v, constants, sizes, arrays):

"Computes a v-greedy policy, returned as a set of indices."

return jnp.argmax(B(v, constants, sizes, arrays), axis=2)

get_greedy = jax.jit(get_greedy, static_argnums=(2,))

Define the \(\sigma\)-policy operator.

def T_σ(v, σ, constants, sizes, arrays):

"""The σ-policy operator."""

# Unpack model

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

r_σ = compute_r_σ(σ, constants, sizes, arrays)

# Compute the array v[σ[i, j], jp]

zp_idx = jnp.arange(z_size)

zp_idx = jnp.reshape(zp_idx, (1, 1, z_size))

σ = jnp.reshape(σ, (y_size, z_size, 1))

V = v[σ, zp_idx]

# Convert Q[j, jp] to Q[i, j, jp]

Q = jnp.reshape(Q, (1, z_size, z_size))

# Calculate the expected sum Σ_jp v[σ[i, j], jp] * Q[i, j, jp]

Ev = jnp.sum(V * Q, axis=2)

return r_σ + β * Ev

T_σ = jax.jit(T_σ, static_argnums=(3,))

Next, we want to computes the lifetime value of following policy \(\sigma\).

This lifetime value is a function \(v_\sigma\) that satisfies

We wish to solve this equation for \(v_\sigma\).

Suppose we define the linear operator \(L_\sigma\) by

With this notation, the problem is to solve for \(v\) via

In vector for this is \(L_\sigma v = r_\sigma\), which tells us that the function we seek is

JAX allows us to solve linear systems defined in terms of operators; the first step is to define the function \(L_{\sigma}\).

def L_σ(v, σ, constants, sizes, arrays):

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

# Set up the array v[σ[i, j], jp]

zp_idx = jnp.arange(z_size)

zp_idx = jnp.reshape(zp_idx, (1, 1, z_size))

σ = jnp.reshape(σ, (y_size, z_size, 1))

V = v[σ, zp_idx]

# Expand Q[j, jp] to Q[i, j, jp]

Q = jnp.reshape(Q, (1, z_size, z_size))

# Compute and return v[i, j] - β Σ_jp v[σ[i, j], jp] * Q[j, jp]

return v - β * jnp.sum(V * Q, axis=2)

L_σ = jax.jit(L_σ, static_argnums=(3,))

Now we can define a function to compute \(v_{\sigma}\)

def get_value(σ, constants, sizes, arrays):

# Unpack

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

r_σ = compute_r_σ(σ, constants, sizes, arrays)

# Reduce L_σ to a function in v

partial_L_σ = lambda v: L_σ(v, σ, constants, sizes, arrays)

return jax.scipy.sparse.linalg.bicgstab(partial_L_σ, r_σ)[0]

get_value = jax.jit(get_value, static_argnums=(2,))

We use successive approximation for VFI.

def successive_approx_jax(T, # Operator (callable)

x_0, # Initial condition

tol=1e-6, # Error tolerance

max_iter=10_000): # Max iteration bound

def body_fun(k_x_err):

k, x, error = k_x_err

x_new = T(x)

error = jnp.max(jnp.abs(x_new - x))

return k + 1, x_new, error

def cond_fun(k_x_err):

k, x, error = k_x_err

return jnp.logical_and(error > tol, k < max_iter)

k, x, error = jax.lax.while_loop(cond_fun, body_fun, (1, x_0, tol + 1))

return x

successive_approx_jax = jax.jit(successive_approx_jax, static_argnums=(0,))

For OPI we’ll add a compiled routine that computes \(T_σ^m v\).

def iterate_policy_operator(σ, v, m, params, sizes, arrays):

def update(i, v):

v = T_σ(v, σ, params, sizes, arrays)

return v

v = jax.lax.fori_loop(0, m, update, v)

return v

iterate_policy_operator = jax.jit(iterate_policy_operator,

static_argnums=(4,))

Finally, we introduce the solvers that implement VFI, HPI and OPI.

def value_function_iteration(model, tol=1e-5):

"""

Implements value function iteration.

"""

params, sizes, arrays = model

vz = jnp.zeros(sizes)

_T = lambda v: T(v, params, sizes, arrays)

v_star = successive_approx_jax(_T, vz, tol=tol)

return get_greedy(v_star, params, sizes, arrays)

For OPI we will use a compiled JAX lax.while_loop operation to speed execution.

def opi_loop(params, sizes, arrays, m, tol, max_iter):

"""

Implements optimistic policy iteration (see dp.quantecon.org) with

step size m.

"""

v_init = jnp.zeros(sizes)

def condition_function(inputs):

i, v, error = inputs

return jnp.logical_and(error > tol, i < max_iter)

def update(inputs):

i, v, error = inputs

last_v = v

σ = get_greedy(v, params, sizes, arrays)

v = iterate_policy_operator(σ, v, m, params, sizes, arrays)

error = jnp.max(jnp.abs(v - last_v))

i += 1

return i, v, error

num_iter, v, error = jax.lax.while_loop(condition_function,

update,

(0, v_init, tol + 1))

return get_greedy(v, params, sizes, arrays)

opi_loop = jax.jit(opi_loop, static_argnums=(1,))

Here’s a friendly interface to OPI

def optimistic_policy_iteration(model, m=10, tol=1e-5, max_iter=10_000):

params, sizes, arrays = model

σ_star = opi_loop(params, sizes, arrays, m, tol, max_iter)

return σ_star

Here’s HPI

def howard_policy_iteration(model, maxiter=250):

"""

Implements Howard policy iteration (see dp.quantecon.org)

"""

params, sizes, arrays = model

σ = jnp.zeros(sizes, dtype=int)

i, error = 0, 1.0

while error > 0 and i < maxiter:

v_σ = get_value(σ, params, sizes, arrays)

σ_new = get_greedy(v_σ, params, sizes, arrays)

error = jnp.max(jnp.abs(σ_new - σ))

σ = σ_new

i = i + 1

print(f"Concluded loop {i} with error {error}.")

return σ

model = create_investment_model()

constants, sizes, arrays = model

β, a_0, a_1, γ, c = constants

y_size, z_size = sizes

y_grid, z_grid, Q = arrays

print("Starting HPI.")

%time σ_star_hpi = howard_policy_iteration(model).block_until_ready()

# Now time it without compile time

start = time()

σ_star_hpi = howard_policy_iteration(model).block_until_ready()

hpi_without_compile = time() - start

print(σ_star_hpi)

print(f"HPI completed in {hpi_without_compile} seconds.")

Concluded loop 1 with error 50.

Concluded loop 2 with error 26.

Concluded loop 3 with error 17.

Concluded loop 4 with error 10.

Concluded loop 5 with error 7.

Concluded loop 6 with error 4.

Concluded loop 7 with error 3.

Concluded loop 8 with error 1.

Concluded loop 9 with error 1.

Concluded loop 10 with error 1.

Concluded loop 11 with error 1.

Concluded loop 12 with error 0.

[[ 2 2 2 ... 6 6 6]

[ 3 3 3 ... 7 7 7]

[ 4 4 4 ... 7 7 7]

...

[82 82 82 ... 86 86 86]

[83 83 83 ... 86 86 86]

[84 84 84 ... 87 87 87]]

HPI completed in 0.14906787872314453 seconds.

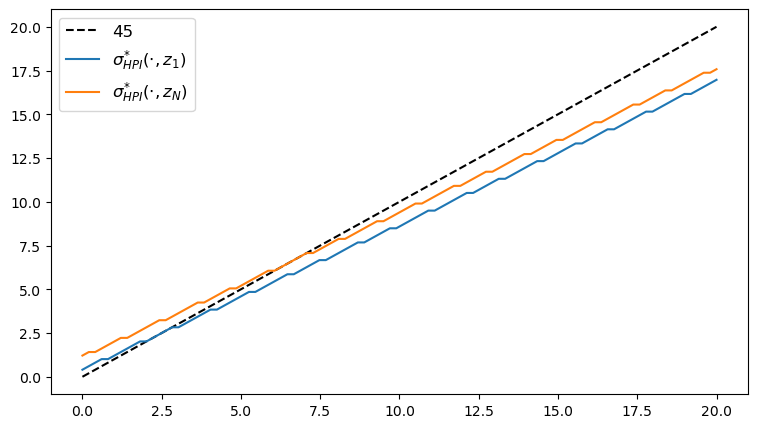

Here’s the plot of the Howard policy, as a function of \(y\) at the highest and lowest values of \(z\).

fig, ax = plt.subplots(figsize=(9, 5))

ax.plot(y_grid, y_grid, "k--", label="45")

ax.plot(y_grid, y_grid[σ_star_hpi[:, 1]], label="$\\sigma^{*}_{HPI}(\cdot, z_1)$")

ax.plot(y_grid, y_grid[σ_star_hpi[:, -1]], label="$\\sigma^{*}_{HPI}(\cdot, z_N)$")

ax.legend(fontsize=12)

plt.show()

print("Starting VFI.")

%time σ_star_vfi = value_function_iteration(model).block_until_ready()

# Now time it without compile time

start = time()

σ_star_vfi = value_function_iteration(model).block_until_ready()

vfi_without_compile = time() - start

print(σ_star_vfi)

print(f"VFI completed in {vfi_without_compile} seconds.")

[[ 2 2 2 ... 6 6 6]

[ 3 3 3 ... 7 7 7]

[ 4 4 4 ... 7 7 7]

...

[82 82 82 ... 86 86 86]

[83 83 83 ... 86 86 86]

[84 84 84 ... 87 87 87]]

VFI completed in 0.51719069480896 seconds.

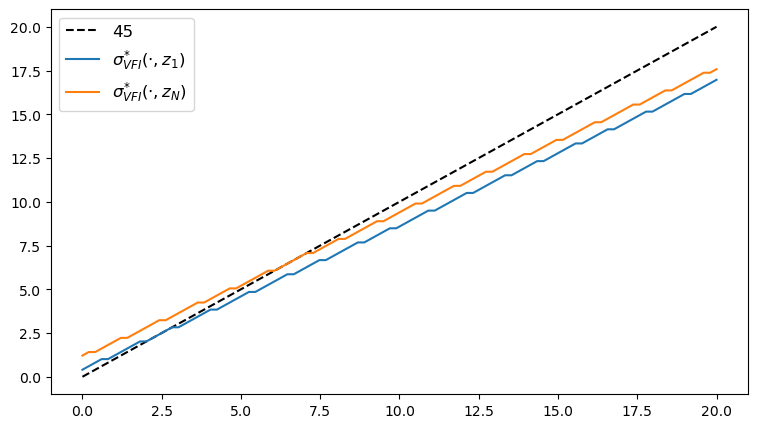

Here’s the plot of the VFI, as a function of \(y\) at the highest and lowest values of \(z\).

fig, ax = plt.subplots(figsize=(9, 5))

ax.plot(y_grid, y_grid, "k--", label="45")

ax.plot(y_grid, y_grid[σ_star_vfi[:, 1]], label="$\\sigma^{*}_{VFI}(\cdot, z_1)$")

ax.plot(y_grid, y_grid[σ_star_vfi[:, -1]], label="$\\sigma^{*}_{VFI}(\cdot, z_N)$")

ax.legend(fontsize=12)

plt.show()

print("Starting OPI.")

%time σ_star_opi = optimistic_policy_iteration(model, m=100).block_until_ready()

# Now time it without compile time

start = time()

σ_star_opi = optimistic_policy_iteration(model, m=100).block_until_ready()

opi_without_compile = time() - start

print(σ_star_opi)

print(f"OPI completed in {opi_without_compile} seconds.")

[[ 2 2 2 ... 6 6 6]

[ 3 3 3 ... 7 7 7]

[ 4 4 4 ... 7 7 7]

...

[82 82 82 ... 86 86 86]

[83 83 83 ... 86 86 86]

[84 84 84 ... 87 87 87]]

OPI completed in 0.2095935344696045 seconds.

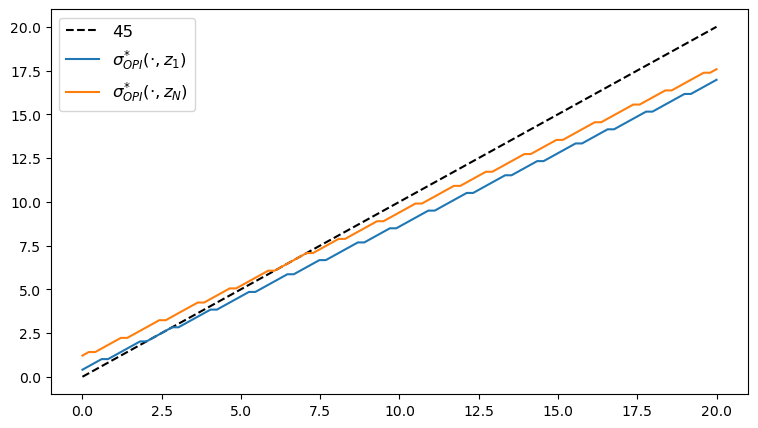

Here’s the plot of the optimal policy, as a function of \(y\) at the highest and lowest values of \(z\).

fig, ax = plt.subplots(figsize=(9, 5))

ax.plot(y_grid, y_grid, "k--", label="45")

ax.plot(y_grid, y_grid[σ_star_opi[:, 1]], label="$\\sigma^{*}_{OPI}(\cdot, z_1)$")

ax.plot(y_grid, y_grid[σ_star_opi[:, -1]], label="$\\sigma^{*}_{OPI}(\cdot, z_N)$")

ax.legend(fontsize=12)

plt.show()

We observe that all the solvers produce the same output from the above three plots.

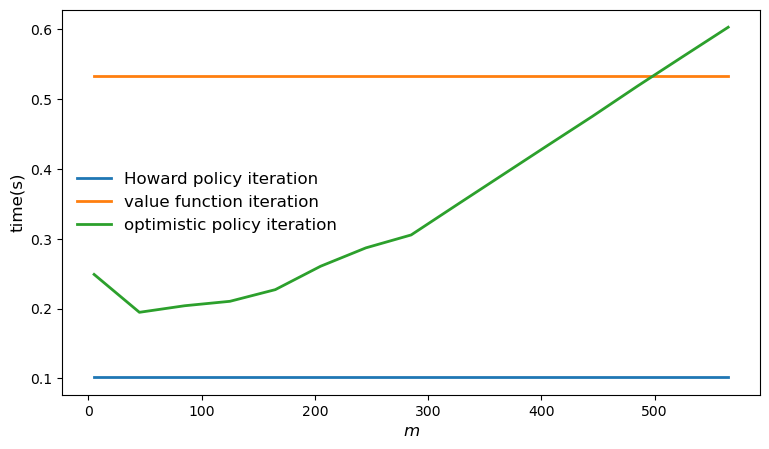

Let’s plot the time taken by each of the solvers and compare them.

m_vals = range(5, 600, 40)

print("Running Howard policy iteration.")

%time σ_hpi = howard_policy_iteration(model).block_until_ready()

Running Howard policy iteration.

Concluded loop 1 with error 50.

Concluded loop 2 with error 26.

Concluded loop 3 with error 17.

Concluded loop 4 with error 10.

Concluded loop 5 with error 7.

Concluded loop 6 with error 4.

Concluded loop 7 with error 3.

Concluded loop 8 with error 1.

Concluded loop 9 with error 1.

Concluded loop 10 with error 1.

Concluded loop 11 with error 1.

Concluded loop 12 with error 0.

CPU times: user 108 ms, sys: 10.9 ms, total: 119 ms

Wall time: 103 ms

# Now time it without compile time

start = time()

σ_hpi = howard_policy_iteration(model).block_until_ready()

hpi_without_compile = time() - start

print(f"HPI completed in {hpi_without_compile} seconds.")

Concluded loop 1 with error 50.

Concluded loop 2 with error 26.

Concluded loop 3 with error 17.

Concluded loop 4 with error 10.

Concluded loop 5 with error 7.

Concluded loop 6 with error 4.

Concluded loop 7 with error 3.

Concluded loop 8 with error 1.

Concluded loop 9 with error 1.

Concluded loop 10 with error 1.

Concluded loop 11 with error 1.

Concluded loop 12 with error 0.

HPI completed in 0.101776123046875 seconds.

print("Running value function iteration.")

%time σ_vfi = value_function_iteration(model, tol=1e-5).block_until_ready()

Running value function iteration.

CPU times: user 576 ms, sys: 11.5 ms, total: 587 ms

Wall time: 530 ms

# Now time it without compile time

start = time()

σ_vfi = value_function_iteration(model, tol=1e-5).block_until_ready()

vfi_without_compile = time() - start

print(f"VFI completed in {vfi_without_compile} seconds.")

VFI completed in 0.5328664779663086 seconds.

opi_times = []

for m in m_vals:

print(f"Running optimistic policy iteration with m={m}.")

σ_opi = optimistic_policy_iteration(model, m=m, tol=1e-5).block_until_ready()

# Now time it without compile time

start = time()

σ_opi = optimistic_policy_iteration(model, m=m, tol=1e-5).block_until_ready()

opi_without_compile = time() - start

print(f"OPI with m={m} completed in {opi_without_compile} seconds.")

opi_times.append(opi_without_compile)

fig, ax = plt.subplots(figsize=(9, 5))

ax.plot(m_vals, jnp.full(len(m_vals), hpi_without_compile),

lw=2, label="Howard policy iteration")

ax.plot(m_vals, jnp.full(len(m_vals), vfi_without_compile),

lw=2, label="value function iteration")

ax.plot(m_vals, opi_times, lw=2, label="optimistic policy iteration")

ax.legend(fontsize=12, frameon=False)

ax.set_xlabel("$m$", fontsize=12)

ax.set_ylabel("time(s)", fontsize=12)

plt.show()